Stay

Stay

Trading Conditions

Products

Tools

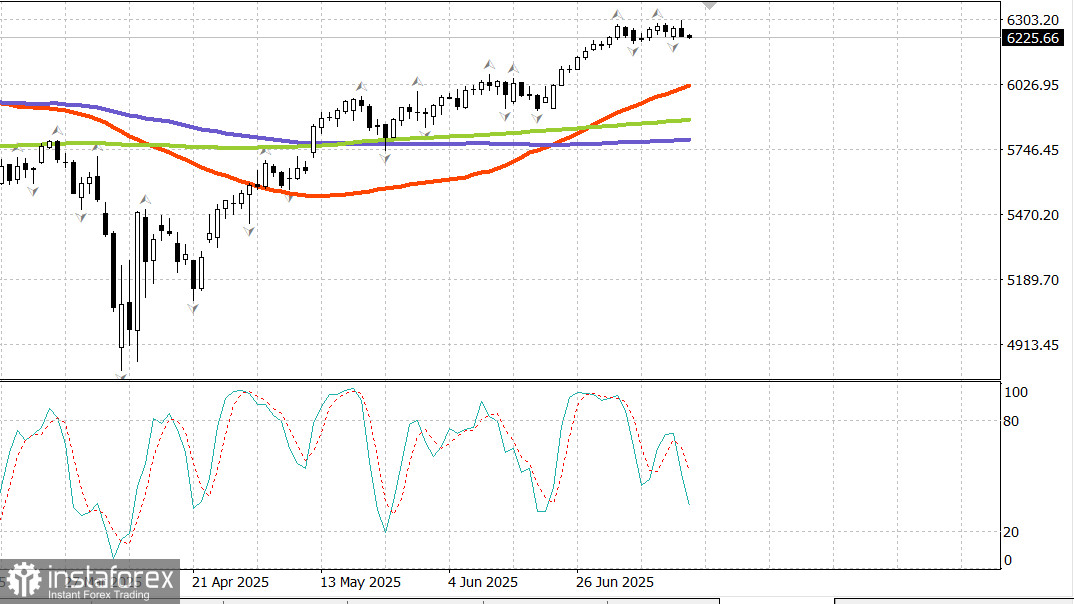

S&P500

Snapshot of US major stock indices on Tuesday

The stock market opened higher on news that NVIDIA (NVDA 170.55, +6.48, +4.0%) would resume sales of its H20 chips in China. However, rising interest rates following the June CPI report created selling pressure, keeping the S&P 500 and broader market under pressure for most of the session.

Thanks to gains in NVIDIA and Advanced Micro Devices (AMD)—which is also aiming to restart AI chip sales in China—the Nasdaq Composite closed at another record high.

The Information Technology sector in the S&P 500 (+1.3%) was the only sector to finish in positive territory. The news on NVIDIA and AMD was further supported by announcements of major investments in AI-powered data centers. For example, Alphabet (GOOG 183.10, +0.29, +0.2%) and CoreWeave (CRWV 140.59, +8.22, +6.2%) announced investments in AI infrastructure. This drove a 1.3% gain in the PHLX Semiconductor Index.

The remaining ten S&P 500 sectors couldn't shake off the pressure from rising interest rates after the June Consumer Price Index (CPI) was released at 8:30 a.m. ET.

The headline CPI rose 0.3% month-over-month in June, and core CPI, which excludes food and energy, rose 0.2%. The latter came in below expectations, which initially boosted the stock market—the S&P 500 briefly hit a new intraday high of 6,302.

However, a deeper dive into the report revealed inflation hotspots in several areas, raising concerns over tariff-driven inflation. For instance, clothing prices rose 0.4% after falling 0.4% in May, while household goods and furnishings prices rose 1.0% after a 0.3% increase in May. Ultimately, the report wasn't strong enough to allay inflation fears, especially those tied to tariffs, which led markets to believe the Fed would maintain its wait-and-see stance.

The Financials sector (-1.7%) finished near session lows. Several major financial firms like JPMorgan Chase (JPM 286.55, -2.15, -0.7%) and BlackRock (BLK 1046.16, -65.30, -5.9%) faced "sell the news" pressure despite beating earnings expectations.

Citigroup (C 90.72, +3.22, +3.7%) was a rare exception to the trend. Meanwhile, Wells Fargo (WFC 78.86, -4.57, -5.5%) disappointed with its forecast for net interest income.

Losses were broad-based on Tuesday: about 90% of S&P 500 stocks declined. While gains in a few major tech names helped mask further downside, the lack of positive news kept the market in a bearish mood following the CPI report.

The Russell 2000 fell 2.0%, the S&P Midcap 400 dropped 1.8%, and the equal-weighted S&P 500 declined 1.4%.

The Treasury market also responded. The yield on the 10-year note rose 6 basis points to 4.49%. Treasury trading remained relatively calm after a batch of Chinese economic data, including a stronger-than-expected Q2 GDP, along with June retail sales, fixed asset investment, and industrial production, which offered a mixed picture relative to expectations.

But calm faded after the June CPI release at 8:30 a.m. ET. Selling pressure swept across the yield curve, driven by inflation concerns and the view that the Fed would treat the CPI report as support for maintaining its cautious stance.

According to the CME FedWatch Tool, the probability of a 25 basis point rate cut (to 4.00–4.25%) at the September FOMC meeting dropped to 54.0%, down from 62.6% the day before.

Following the CPI release, the US dollar strengthened, reflecting the belief that interest rates may stay elevated for longer. The US dollar index rose 0.6% to 98.64.

Boston Fed President Susan Collins (a voting FOMC member) reiterated a monetary policy stance of "active patience" in her remarks.

Energy

Brent crude oil is now trading at $68.80.

Conclusion

The US stock market may be beginning its downward correction. Investors are waiting for correction targets to be reached before buying.

InstaForex analytical reviews will make you fully aware of market trends! Being an InstaForex client, you are provided with a large number of free services for efficient trading.